October 2015 Dashboard

US stocks staged their strongest monthly rally in four years in October, as corporate earnings have mostly surprised on the upside and, later in the month, the Fed raised the prospect of increasing short-term interest rates in December. We have been jilted at the altar of late by the Fed (see: September rate hike head fake), so any indication that after nine years from the last rate hike, they believe the economy can withstand a 0.25% increase in borrowing costs (up from zero) ought to be good news to investors.

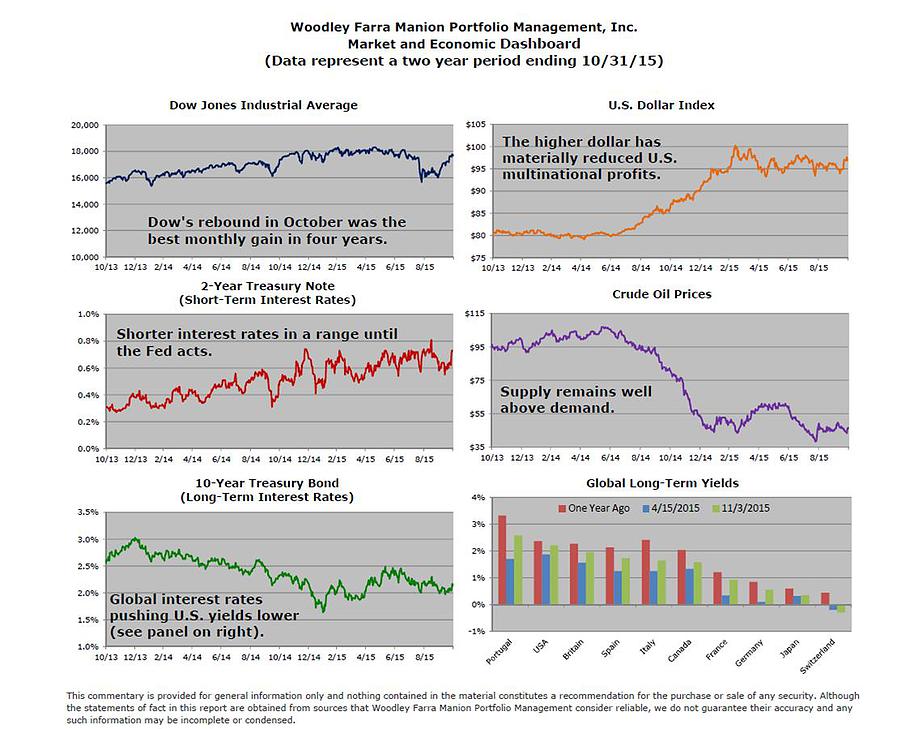

While the Fed has been dithering over a prospective rate hike, central banks around the world have taken the opposite tack and have gunned their bond markets to record-low interest rate levels in the hope of jump-starting their economies. This month’s highlighted chart shows the 10-year interest rate for several Euro Zone countries, as well as Canada, Japan and Britain. Note the US and Britain have the highest yields (save for Portugal), which reflect both countries’ relative success in using Quantitative Easing several years ago. As QE pioneers, the US and Britain have seen better economic growth as well as stronger labor markets. Japan and the Euro Zone have fully embraced QE, meaning their central banks are engineering a sharp drop in longer-term interest rates to reduce borrowing costs and nudge investors to take more risks. Risk-taking is a crucial component of economic growth and shifting investments from safe government bonds to capital spending, stocks, real estate, business formation, etc., is the ultimate goal of QE.

The stock market is now in the October-April time frame that usually produces the best returns for investors. After a sharp drop in the late summer, the market is now close to the highs established earlier in 2015. We’ll see if investors push prices to new highs, or use the rally to reduce their exposure. Since the safe government bond alternative offers poor value, maybe the rally will be durable and we’ll head into year-end on a positive note.