August 2015 Economic Dashboard

We hope your summer is going well, even as the volatile market since late July has put a damper on the season. Stocks suffered their worst month in August in over five years over worries about China’s growth and ongoing debates about the Federal Reserve’s first interest rate hike since 2006.

Following are a few observations now that we are in September, which is traditionally one of the two weaker months in the calendar for the market (August is the other):

1. The Fed continues to loom large; while market volatility may create an argument to hold off on raising the Fed Funds rate in two weeks, labor markets and demand for credit are telling us the economy is improving. The Fed wants to boost inflation expectations and a rate hike is necessary to do so. As a result, investors are trying to digest the coming era of interest rate normalization.

2. China is transitioning from a rapidly industrializing economy to a more mature one. The “command” economy that dictated resources are allocated to certain industries and real estate development may not be the ideal model for an economy that needs to develop more of an internal focus on consumerism and services. China has many levers it can pull to stabilize the economy, though long-run it needs to allow more creative destruction to better allocate resources.

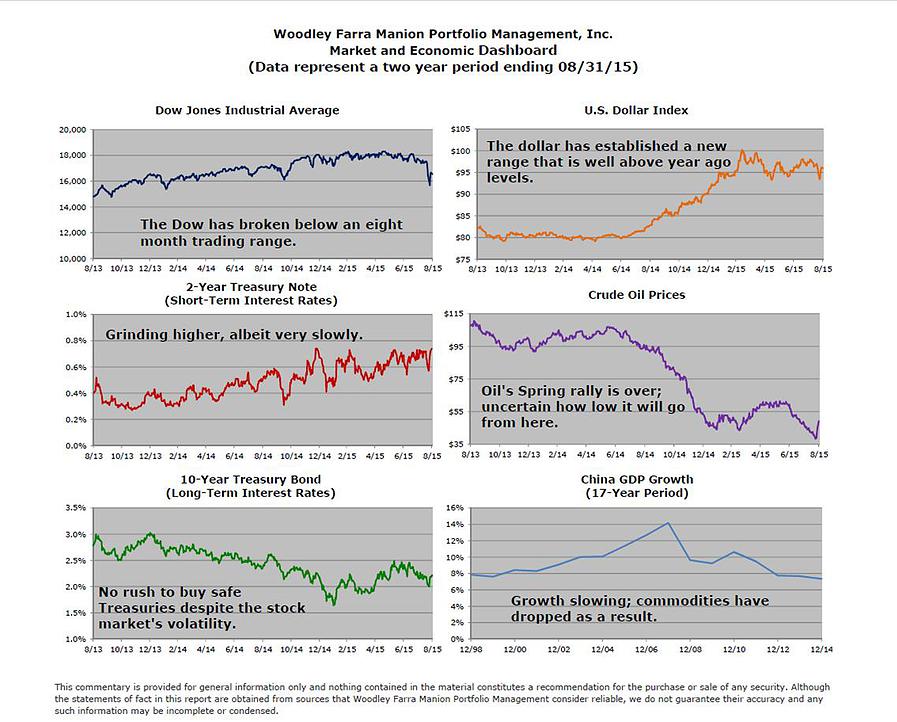

3. Commodity markets have declined significantly as a result of slowing demand in China; those countries that feasted on Chinese demand are now in the doldrums as supplies are too high. But, we view the drop in commodities as a strong positive for the big four regions that are now growing a little stronger (US, UK, Euro Zone and Japan). These four regions represent 56% of global GDP (China is 13%) and they have not grown in unison since the 1980s.

4. Stocks have enjoyed a three year period of strong appreciation and low volatility. The current correction can be viewed as overdue and ultimately will be a restorative tonic for longer term appreciation. We firmly believe the US market is in a secular bull market that will last for several more years. These longer bull markets are punctuated with interim bear markets. This correction could yet develop into a bear market, but looking back in history, interim bear markets tend to be briefer and shallower than what we experienced in 2000-2002 and 2007-2009. Importantly, severe bear markets are associated with recessions, and there is no recession on the horizon in the US.

This commentary is provided for general information only and nothing contained in the material constitutes a recommendation for the purchase or sale of any security. Although the statements of fact in this report are obtained from sources that Woodley Farra Manion Portfolio Management consider reliable, we do not guarantee their accuracy and any such information may be incomplete or condensed.